Suppose the are independent random variables

with values in the unit interval and common mean . Since the

are independent and each only depends on , the

are marginally independent as well. Each takes on

only the values 0 and 1, so the marginal distributions of the

are Bernoulli with success probability

So the are independent Bernoulli() random variables and

therefore

is Binomial(, ). If the

have a Beta(,) distribution then

and therefore

Var

c.

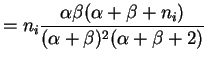

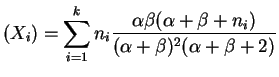

For each

Var

Var Var

Var

Var

Again the are marginally independent, so

Var

Var

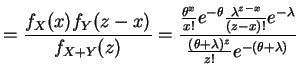

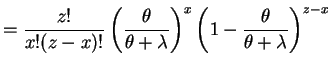

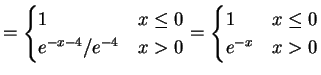

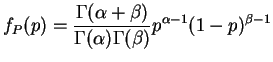

The marginal distribution of is called a beta-binomial

distribution. The density of is

for . So the PMF of is

4.21

Gamma Exponential and

Uniform.

The joint density of

is

for

. The inverse transformation is

This is messy to differentiate; instead, compute

So , and

Thus are independent standard normal variables.

4.28

a.

So

Thus

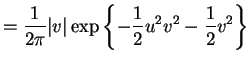

and

This is a Cauchy(1/2,1/2) density.

b.

with

. So

and

4.29

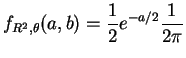

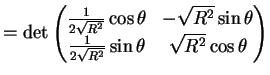

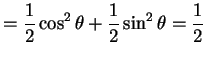

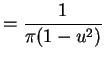

a.

.

is one to one on , and periodic with period

. So

. Since

is uniformly distributed on and is one to one on we have

and

the density of is

which is a standard Cauchy density.

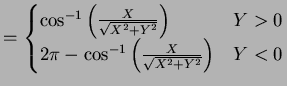

b.

. Since

and

are periodic

with period and since

we have

Since both

and

are

uniformly distributed on this shows that

,

and

all have the same

marginal distribution, and therefore

has the same

distribution as

.

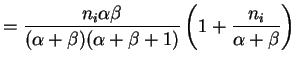

![$\displaystyle = E[E[X_i\vert P_i]] = E[n_iP_i] = n_iE[P_i] = n_i \frac{\alpha}{\alpha+\beta}$](img545.png)

![$\displaystyle = \sum E[X_i] = \frac{\alpha}{\alpha+\beta}\sum_{i=1}^k n_i$](img559.png)

![$\displaystyle = E[P(X_i = x\vert P_i)] = E\left[\binom{n_i}{x}P_i^x(1-P_i)^{n_i-x}\right]$](img565.png)